-

If you are citizen of an European Union member nation, you may not use this service unless you are at least 16 years old.

-

You already know Dokkio is an AI-powered assistant to organize & manage your digital files & messages. Very soon, Dokkio will support Outlook as well as One Drive. Check it out today!

| |

03 Panel Data Analysis Methods

Page history

last edited

by editor 11 years, 5 months ago

Panel Data Analysis

Introduction

Panel data, also called longitudinal data or cross-sectional time series data, are data where same entities (panels) like people, firms, and countries were observed at multiple time points.

- National Longitudinal Survey is an example of panel data, where a sample of people were followed up over the years.

- General Social Survey data, for example, are not longitudinal data although a group of people were surveyed for multiple years, because the respondents are not necessarily the same each year.

Methodology

Setting up STATA database

|

- Obtain your file

- Ex: Open nlswork.dta. Give a command:

. use http://www.stata-press.com/data/r11/nlswork.dta

- Declare that data set is panel

- Indicate

- the name of the panel (idcode)

- the time variables (year)

- Both panel and time variables need to be numeric

- Then type:

. xtset idcode year

OR: Select Statistics -> Longitudinal/panel data -> Setup and Utilities -> Declare dataset to be panel data

Output:

- "Unbalanced" idcode: gaps present among the id numbers

- "Year... but with gaps": no need to do anything

- Other considerations:

- Create a numeric code for any string panel variable (Ex: string date --> Stata date format

- Data should like this

Panel ID Time Variable Var3 Var4 Var5...

1 1978 .. .. ..

2 1979

3 1980

4 1981

(unique) (Stata date)

(numeric) (numeric)

|

Entity Fixed Effects

|

|

Application:

- It helps to control for omitted variables that differ among panels, but are constant over time

Example: Effect of 'experience' on 'earning'

- Here, earning (wage) obviously is influenced by factors other than experience (tenure), such as personality of the person, which can be assumed to stay constant over time

- With this assumption of fixed entity (other than 'experience') we can run a fixed effects regression with the following model:

Then the model will be:

- ln(Wage) = intercept + b1*(TenureForEachPanel&Time) + b2*(UnobservedCharacteristicsForEachPanel) + ErrorForEachPanel&Time

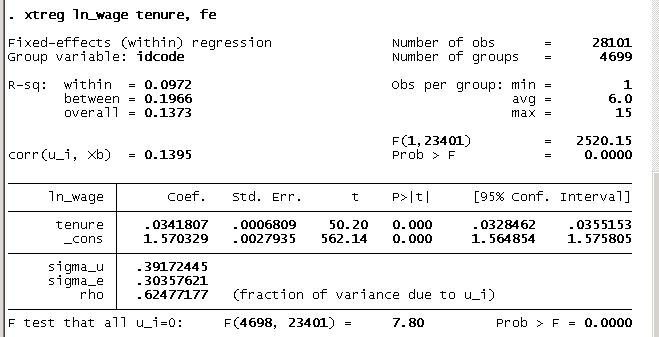

. xtreg ln_wage tenure, fe

- xtreg is used for panel data

- fe indicates other variables have fixed effect

- OR: select Statistics -> Longitudinal/panel data -> Linear models -> Linear regression (FE,RE,PA,BE)

- Output:

- The output shows you that it is a fixed-effects regression, with a group variable idcode.

- There is a total of 28,101 observations, and 4,699 groups (persons in this case)

- The observations per group, in this case year, ranges from 1 to 15. Plugging in the coefficients into the above model, we have:

|

Time Fixed Effects

|

|

In this method, we assume that the unobserved effects vary across time rather than individuals (or persons - such as personality in previous example). Ex: national economy may impact everyone the same way but it varies across times (ex: in y1 it may be low and in y3 it may be higher). So to control for 'national economy' in a model, we can run time fixed effects regression model:

- Log(Wage) = (interceptForEachTime) + b1*(TenureForEachPanel&Time) + (ErrorForEachPanel&Time)

- So, the intercept includes the variation of time rather than panels. Estimation model will then be:

EstimatedLogWage = (TimeFixedEffects) + b1*(TenureForEachPanel&Time)

STATA Command:

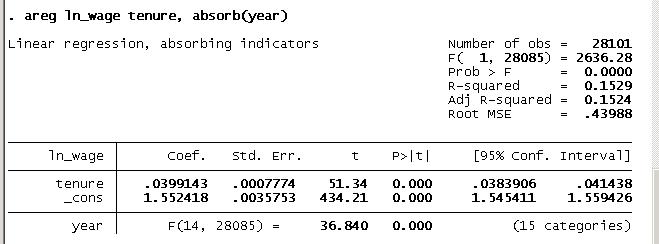

. areg ln_wage tenure, absorb(year)

- areg is used to run fixed effect

- year is indicated as the variable to be absorbed

- OR Statistics -> Linear models and related -> Other -> Linear regression absorbing one cat. variable

STATA Output:

- By plugging in these coefficients, we have

EstimatedLogWage = 1.55 + 0.039TenureForEachPanel&Time

- As in the case of entity fixed effects, you can include t-1 dummy variables in the model, where t is the total number of years in the data.

- tabulate command with generate option creates a dummy variable for each year.

- Using asterisk (*) with yr, you can include yr1 through yr15.

- If you include a constant, then the constant takes the effect of the year that is ommitted.

- Here we purposefully exclude the constant.

- In the areg, the constant absorbed all the year's effects, whereas in the dummy version, you'll have an intercept for each year.

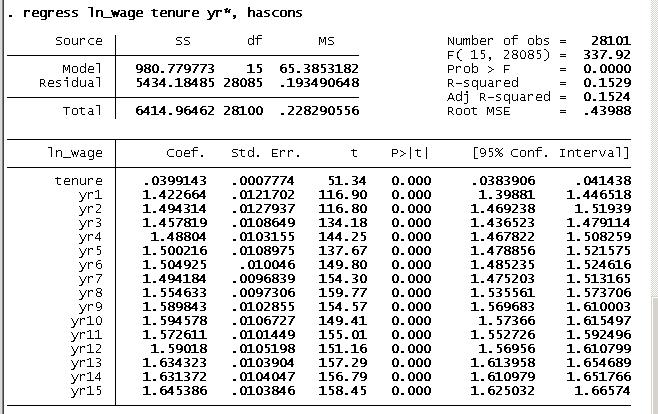

Dummy method (as opposed to areg)

. tabulate year, generate(yr)

. regress ln_wage tenure yr*, hascons

- Notice that the coefficient, standard error, and t-value of tenure are the same as in areg results.

- In time fixed effects model, we assumed that the slope for tenure is the same for all years but the intercept is different.

- If you think that there not only are effects that are different for each year, the effect of tenure would also be different for each year, you may run regressions for each year.

. sort year

. by year: regress ln_wage tenure

|

Random Effects Regression

|

|

Application:

- When some omitted variables may be constant over time but vary among panels, and others may be fixed among panels but vary over time

STATA

Stata's RE estimator is a weighted average of fixed and between effects models.

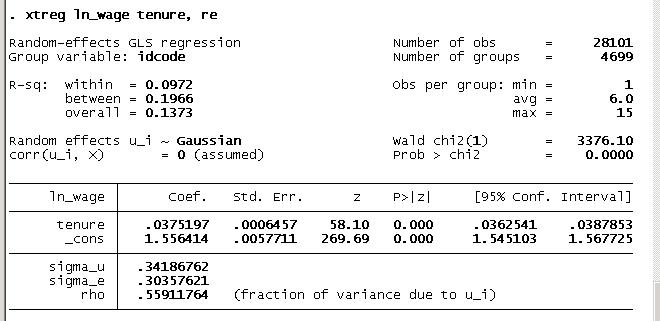

. xtreg ln_wage tenure, re

- Estimated regression outcome is:

- EstimatedLogWage = 1.55 + 0.0375TenureForEachPanel&Time

|

Choosing between Fixed-effect & Random-effect regressions

|

|

Perform Hausman test

- Save the coefficients from each of the models and use the stored results in the test

. xtreg ln_wage tenure, fe

. estimates store fixed

. xtreg ln_wage tenure, re

. estimates store random

. hausman fixed random

OR: Statistics -> Postestimation -> Tests -> Hausman specification test

---- Coefficients ----

| (b) (B) (b-B) sqrt(diag(V_b-V_B))

| fixed random Difference S.E.

-------------+----------------------------------------------------------------

tenure | .0341807 .0375197 -.0033389 .0002159

------------------------------------------------------------------------------

b = consistent under Ho and Ha; obtained from xtreg

B = inconsistent under Ha, efficient under Ho; obtained from xtreg

Test: Ho: difference in coefficients not systematic

chi2(1) = (b-B)'[(V_b-V_B)^(-1)](b-B)

= 239.11

Prob>chi2 = 0.0000

|

Hausman Test:

- It tests the null hypothesis that RE and FE estimated coefficients are the SAME. So if they are same then use FE; if they are not same then use RE

P-value is significant (=different)

=> Use FE

RULE:

- Use RE: If NOT significant P-value

- Use FE if: If Significant P-value

RATIONALE:

- The Hausman test tests the null hypothesis that the coefficients estimated by the efficient random effects estimator are the same as the ones estimated by the consistent fixed effects estimator.

- If you get a statistically significant P-value, however, you should use fixed effects.

|

|

Between Effects Regression

|

|

Application

This model is similar to taking the mean of each variable in the model for each panel across time and running a regression on the collapsed data set of means

STATA

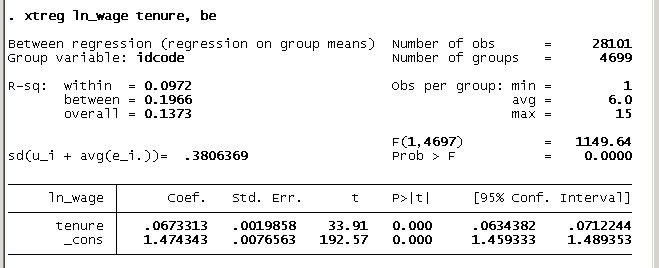

. xtreg ln_wage tenure, be

- In this data, some people's tenure information is missing

- In xt command, Stata will automatically exclude missing values from the computations.

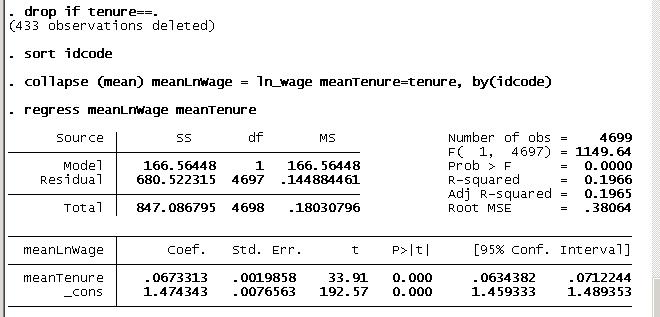

Alternatively (more-work-version):

- Manually creating means with collapse, however, will not automatically exclude missing values.

- So we need to remove the cases with missing tenure before collapsing.

. drop if tenure == .

. sort idcode

. collapse (mean) meanLnWage=ln_wage meanTenure=tenure, by(idcode)

. regress meanLnWage meanTenure

- The number of observations in the second regression matches the number of groups in xt regression.

- It created identical result as in the xt result above.

|

References

Contents adapted from: http://dss.wikidot.com/panel-data-analysis

- Stata Longitudinal/Panel-Data Reference Manual Release 11. Stata Press.

- Stock, James H. and Watson, Mark W. 2007. "Chapter 10 Regressino with Panel Data" in Introduction to Econometrics. Second Edition. Pearson Education, Inc.

- UCLA Academic Technology Services. Using xtreg. http://www.ats.ucla.edu/stat/stata/code/xt.htm ; retrieved August, 2010.

- UCLA Academic Technology Services. Stata FAQ: What is the relationship between xtreg-re, xtreg-fe, and xtreg-be? http://www.ats.ucla.edu/stat/stata/faq/revsfe.htm ; retrieved August, 2010.

03 Panel Data Analysis Methods

|

|

Tip: To turn text into a link, highlight the text, then click on a page or file from the list above.

|

|

|

|

|

Comments (0)

You don't have permission to comment on this page.